What is Blockchain Technology and How Does it Work?

We’re reader-supported; we may earn a commission from links in this article.

Blockchain technology has recently gained popularity as a secure and transparent way to conduct transactions and store data.

This revolutionary technology can potentially transform many industries, from finance to healthcare.

In this article, we will explore the basics of blockchain technology, how it works, and its potential applications.

1. What is Blockchain Technology?

Blockchain technology is a digital ledger that records transactions in a decentralized and transparent manner.

The technology is based on a distributed ledger, which means the data is replicated across multiple nodes in a network, making it almost impossible to tamper with.

Bitcoin was the first application of blockchain technology and remains the most well-known. It operates on a public ledger that allows anyone to participate.

However, private blockchain networks also exist, which are restricted to a specific group of participants – they are typically used for internal business processes, offering more control and privacy to the participants.

Overall, the distributed ledger technology that powers blockchain networks has the potential to revolutionize how transactions are conducted, providing increased security, transparency, and efficiency for traditional business networks.

i. What is a blockchain protocol?

The blockchain protocol is the set of rules governing how the blockchain network operates, ensuring that all participants follow the same rules.

ii. History of Blockchain Technology

The origins of blockchain technology can be traced back to the early 1990s when researchers attempted to create a decentralized digital currency system.

However, it was not until 2008 that the first full blockchain system was introduced. Satoshi Nakamoto, the creator of Bitcoin, published a paper that described a decentralized, peer-to-peer electronic cash system.

The system relied on a distributed ledger, which came to be known as the blockchain.

Over the years, blockchain technology has evolved significantly. Today, it is being used in various applications beyond cryptocurrency, such as developing blockchain applications such as supply chain management, digital identity verification, smart contracts, and even voting systems.

iii. How Does Blockchain Technology Work?

Blockchain technology is a decentralized ledger that is maintained by a network of nodes.

Each node has a copy of the ledger, and transactions are verified by consensus among the nodes.

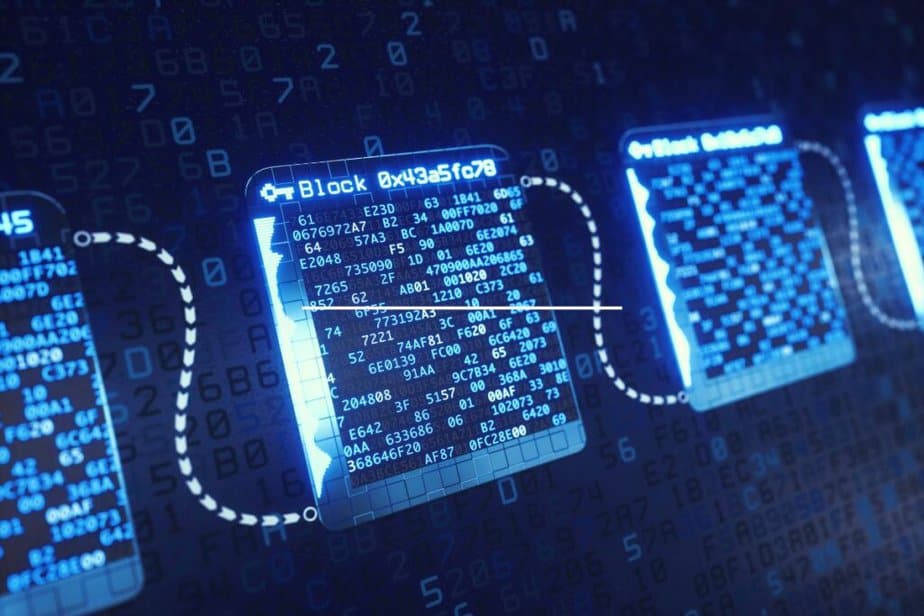

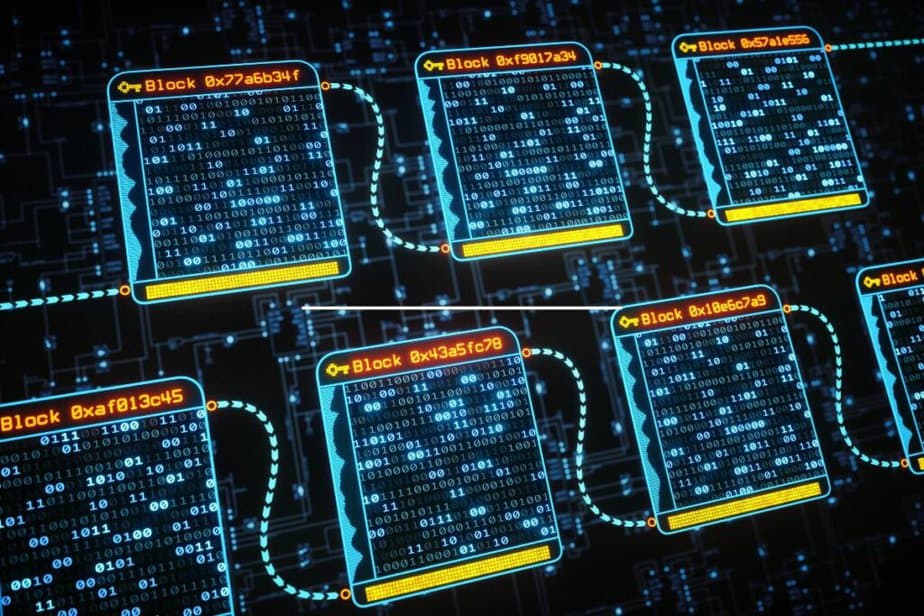

When a transaction is made, it is added to the blockchain as a new block. Each block contains a cryptographic hash of the previous block, creating a chain of blocks that cannot be altered without consensus from the network.

The blockchain’s decentralized nature ensures that no central authority controls the ledger, making it resistant to fraud and hacking attempts.

Moreover, the transparency of the blockchain and distributed database makes it easier for blockchain users to trace transactions and identify suspicious activities.

iv. Applications of Blockchain Technology

Blockchain technology has found various applications beyond cryptocurrency.

For instance, it can be used in supply chain management to track the movement of goods from one single point of failure to another.

It can also be used in digital identity verification to create a secure and tamper-proof system for verifying identities.

Blockchain technology can also be used in voting systems to create a transparent and secure system that ensures the integrity of the voting process.

By providing a decentralized and transparent platform, blockchain technology offers a level of trust and security that was previously impossible.

2. Types of Blockchain

Blockchain technology has rapidly gained traction over the years, with various types of various blockchain protocols emerging to cater to different industries and applications.

Here are a few types of blockchains you should know:

a. Public Blockchain

A public blockchain is an open network accessible to anyone who wants to participate. It is entirely decentralized; anyone can read, write, or audit the blockchain.

Transactions are verified by consensus among the nodes, which ensures that the network is secure and resistant to fraudulent activities.

Public blockchains are typically used in cryptocurrencies, where transparency and decentralization are crucial for maintaining trust in the proof-of-work network. As no central authority controls the ledger, public blockchains are more resistant to hacking attempts and fraud.

b. Private Blockchain

On the other hand, a private blockchain is a closed network that is only accessible to a select group of participants.

Transactions are still verified by consensus among the nodes, but the participants control access to the network.

Private blockchains are typically used in industries where privacy and confidentiality are paramount, such as healthcare and finance.

By restricting access to the network, private blockchains provide a more secure and controlled environment for transactions.

c. Consortium Blockchain

A consortium blockchain is a hybrid of public and private blockchains.

A group of participants controls a consortium blockchain, but it is still open to anyone who wants to participate in the network.

Transactions are verified by consensus among the nodes, and the consortium controls access to the network.

Consortium blockchains are typically used in industries where collaboration is essential, such as supply chain management.

By providing blockchain platforms with a more transparent and controlled environment for transactions and business networks, consortium blockchains allow multiple organizations to work together in a secure and trusted manner.

3. Benefits of Blockchain Technology

Blockchain technology is a transformative innovation that has disrupted various industries. Here are a few benefits of blockchain technology:

a. Security

One of the primary benefits of blockchain technology is its security. Blockchain technology uses cryptographic algorithms to secure the decentralized network.

Transactions are verified by consensus among the nodes, making it difficult for malicious actors to manipulate the blockchain.

This makes the blockchain platform a more secure option for transactions, particularly in the digital space where fraud and hacking attempts are prevalent.

b. Transparency

Another benefit of blockchain, blockchain distributed ledger technology, is its transparency.

The blockchain is a decentralized ledger, so anyone can audit the network and verify transactions.

This creates high transparency and accountability, making it easier to trace transactions and identify suspicious activities.

c. Decentralization

The blockchain is a decentralized ledger, which means that any single entity does not control it. This makes it more resilient to attacks and more resistant to censorship.

The decentralization of the blockchain also ensures that no central authority controls the ledger, making it a more democratic and equitable system.

d. Efficiency

Blockchain technology can be more efficient than traditional systems because it eliminates the need for intermediaries.

Transactions can be processed faster and at a lower cost. By removing intermediaries, blockchain technology streamlines the transaction process, making it more efficient and cost-effective.

e. Lower Costs

Another benefit of blockchain technology is its ability to reduce costs associated with financial transactions.

As blockchain technology eliminates the need for intermediaries, it can reduce costs such as fees charged by banks or other financial institutions.

This makes it a more cost-effective option for transactions, particularly in industries where transaction fees and costs can be a significant burden.

4. Applications of Blockchain Technology

Blockchain technology is already in use today in various sectors over the past few years.

Here are a few ways blockchains are applied in real life:

a. Cryptocurrency

The most well-known application of blockchain technology is cryptocurrency.

Bitcoin was the first cryptocurrency, but thousands of cryptocurrencies are now in circulation.

Cryptocurrencies use blockchain technology to create a decentralized system for conducting transactions.

b. Supply Chain Management

Blockchain technology can create a transparent and secure supply chain management system.

By using a blockchain-based supply chain system, companies can track products from the point of origin to the point of sale, reducing the risk of fraud or counterfeiting.

c. Voting Systems

Blockchain technology can be used to create a secure and transparent voting system.

Using a blockchain-based system, votes can be recorded and verified in a secure way that cannot be manipulated.

d. Healthcare

Blockchain technology can be used to create a secure and transparent system for managing healthcare records.

By using a blockchain-based system, patients can have greater control over their healthcare data, and healthcare providers can ensure the integrity and security of patient information.

e. Real Estate

Blockchain technology can create a secure and transparent system for managing real estate transactions.

Using a blockchain-based system to record transactions, property ownership can be verified, and transactions can be processed more efficiently.

f. Intellectual Property

Blockchain technology can be used to create a secure and transparent system for managing intellectual property.

By using digital assets to validate transactions using a blockchain-based system, creators can protect their intellectual property and ensure they receive proper credit and compensation for their work.

5. Challenges of Blockchain Technology

While blockchain technology has numerous benefits, it also faces challenges that hinder its widespread adoption.

Here are some major challenges facing blockchain technology: regulation, adoption, scalability, and interoperability.

a. Regulation

One of the biggest challenges facing blockchain technology is regulation.

Many governments are still trying to figure out how to regulate blockchain-based systems, which can be difficult because the technology is so new.

Regulations are necessary to ensure blockchain-based systems comply with legal and regulatory requirements and prevent fraudulent activities.

However, over-regulation can stifle innovation and limit the growth of the blockchain ecosystem.

b. Adoption

Another significant challenge facing blockchain technology is adoption.

While the technology has the potential to transform many industries, it is still relatively new, and many businesses and consumers are hesitant to adopt it.

The lack of standardization, education, and awareness around blockchain technology can hinder its adoption.

c. Scalability

Scalability is another challenge facing blockchain technology.

As more transactions are added to the public blockchain networks, the network can become slower and less efficient.

This is because each node in the public blockchain network has to verify every transaction, which can slow down the process as the network grows.

To overcome this challenge, developers are exploring various solutions, such as sharding, sidechains, and off-chain transactions.

d. Interoperability

Interoperability is another challenge facing blockchain technology.

Because there are so many different blockchain-based systems, it can be difficult for them to work together seamlessly.

This can limit the effectiveness of existing blockchain-based systems and hinder their adoption. Interoperability solutions such as cross-chain bridges and middleware are being developed to address this challenge.

Conclusion

Blockchain technology is a revolutionary technology that has the potential to transform many industries.

Its benefits include security, transparency, decentralization, efficiency, and lower costs. It has applications in cryptocurrency, supply chain management, voting systems, healthcare, real estate, and intellectual property.

However, there are also challenges facing blockchain technology, including regulation, adoption, scalability, and interoperability.

Despite these challenges, the potential benefits of blockchain technology make it a technology worth exploring.

FAQs

What is a blockchain node?

A blockchain node is a computer that is connected to the blockchain network. Nodes are responsible for verifying, recording transactions, and maintaining the blockchain.

Can blockchain technology be hacked?

While it is technically possible for Bitcoin blockchain and technology to be hacked, it is extremely difficult due to the decentralized and secure nature of the technology.

What is a smart contract?

A smart contract is a self-executing contract that is stored on the blockchain. It automatically executes the terms of the contract when certain conditions are met.

What is a 51% attack?

A 51% attack is a type of attack on a private blockchain network where a single entity controls more than 50% of the network’s computing power. This can allow the entity to manipulate transactions on the entire blockchain itself.

What is the difference between a public and private blockchain?

A public blockchain is a decentralized database open to anyone who wants to participate in the network, while a private blockchain is only accessible to a select group of participants.

What is blockchain, and how does it work for dummies?

The Bitcoin-based blockchain allows storing and processing bitcoins in shared, distributed ledgers, but this shared ledger can record all transactions and track any assets, whether tangible, intangible, or digital.

Blockchains allow the settlement of a stock transaction within hours rather than a few days.

Justin Chia

Justin is the author of Justjooz and is a data analyst and AI expert. He is also a Nanyang Technological University (NTU) alumni, majoring in Biological Sciences.

He regularly posts AI and analytics content on LinkedIn, and writes a weekly newsletter, The Juicer, on AI, analytics, tech, and personal development.

To unwind, Justin enjoys gaming and reading.